Larger Headcount And Steep Labor Costs Key Reasons For Price Pressure Within Supply Chains

Trucking firms are in the midst of a conundrum with recruiting and retaining labor, even as the fate of the peak freight season hangs in the balance.

Welcome to The Logistics Report, a weekly newsletter that discusses anything logistics. This is a space where we dissect market trends, chat with industry thought leaders, highlight supply chain innovation, celebrate startups, and share news nuggets.

It is always a good time to talk about the trucking industry. While the trucking market has been seeing a few green shoots of demand in the recent weeks leading up to the peak season, trends are neither strong nor convincing enough. But the same can’t be said of trucking employment. FRED data on truck transportation employment numbers has shown a steady increase to 1.62 million in July — touching its all-time high from Oct ‘22.

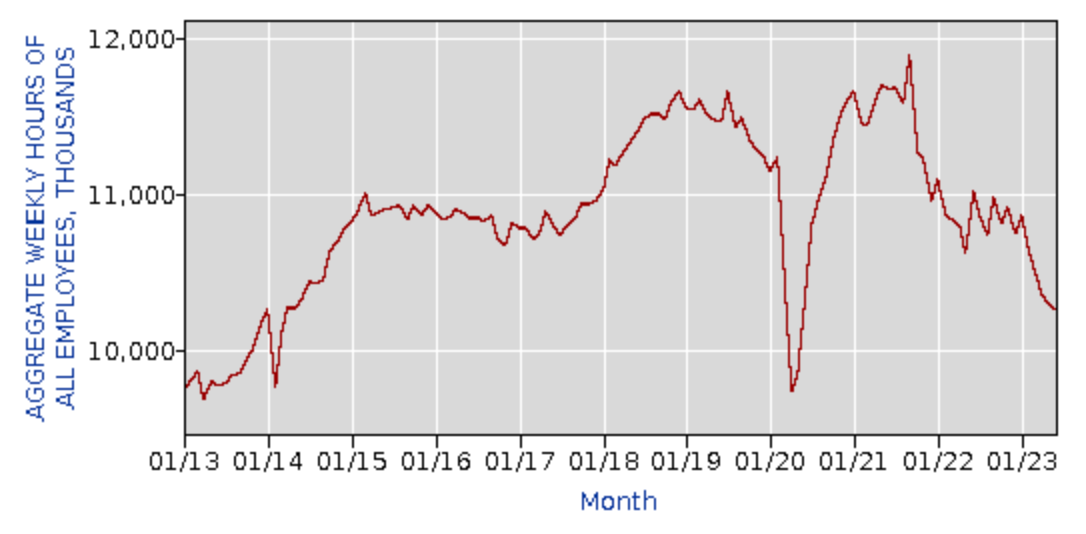

While transportation jobs month-over-month growth in July was underwhelming compared to the month before, it still does not discount the size of the industry workforce today. And considering freight volumes and profit margins have dipped significantly since the last headcount peak in Oct ‘22, it is quite interesting to see trucking firms continuing to recruit and retain labor. This, despite clear data on the reduced workload for trucking employees. Bureau of Labor Statistics data on employment hours of all trucking employees has continued to fall all through ‘23 since peaking in Q3 ‘22.

A lot can be gleaned by putting this together. For one, it is quite possible that trucking firms are beginning to sense the dawning of a better freight market situation as volumes tick up and freight rates bounce off their floor.

Conversely, the fervent recruiting of trucking labor can also signify carriers’ issues with finding good truck drivers to join their fleet. The pandemic-driven retail boom generated an explosive surge in trucking needs, spiking driver demand. As truck driving (specifically long-haul) isn’t very glamorous, a chunk of these drivers moved out to less-taxing last-mile operations or to other verticals in the supply chain. Some of these drivers departed large trucking firms they were working with, building their own trucking establishments during the historically tight market to run in the spot, looking to make hay while the sun shone.

This fashioned up as an ugly situation for large trucking carriers — a higher-than-usual driver churn rate during a period when they could make money hand over fist. Then again, the cyclical market has turned fortunes, driving trucking establishments (especially owner-operators and small firms) out in droves as low freight rates and high operational costs have forced them to shutter doors.

As the industry sobers up from the pandemic freight peak, trucking carriers that weathered the storm are now better positioned to attract returning drivers. While it is still hazy about how the peak retail season will turn out this year, peaking trucking industry recruitment numbers coupled with falling industry-wide work hours make it seem like carriers are backing themselves into a corner.

Another argument is that the truckload sector is unwilling to give up on its workforce, as it is hard to build a good driver base. “There’s also the fact that the median age in the industry tends to be higher in the late 40s,” said Matt Muenster, chief economist at Breakthrough. “I imagine firms retaining drivers with that in mind — recognizing and maintaining talent is difficult. Despite headwinds in the market, I believe we’ve seen through the worst of it in the first half of ‘23.”

The economy has been robust at large, with the unemployment rate falling by 0.1% month-over-month to 3.5% in July — further underscoring the persistent labor market pressure.

“Notably, both the household and establishment surveys have trends that align. This contrasts the previous month, where there was a marked divergence between these two key indicators,” said Muenster. “The fact that these numbers are moving in the same direction reinforces the notion that labor market tightness remains unchanged and is not showing signs of easing.”

To keep this story in balance, it makes sense to check consumer retail demand. While record-low unemployment rates have meant consumers have largely continued to spend liberally, the avenues to where they channel their money have seen a gradual, but expected, shift. Consumers now spend more on services than on retail, with the services sector making a return after being heavily repressed during the pandemic. Considering every dollar spent on services generates less freight volume than every dollar spent on retail, a growing GDP masks the real plight of the freight economy.

Regardless, retail demand has remained fairly strong considering the pre-pandemic yardstick. Yet, a lot of this ‘demand’ did not translate into trucking activity as a significant part of it was inventories retailers were downsizing from their saturated warehouses and overstocked stores, rather than fresh orders from manufacturers and suppliers. This existing inventory glut meant that even as consumers purchased goods, trucks weren't as active in moving new stock, leading to a mismatch between retail sales and trucking demand.

Strictly speaking, retail demand is regressing to its mean from the pre-pandemic years. Nonetheless, the steep fall in demand from the ‘22 peak is taking some time to get used to. “Inflation is slowly getting under control, but we’ll have other factors like elevated interest rates that will influence how consumers spend on housing. The student loan repayment restarts will also impact retail demand,” pointed out Muenster.

While a loose freight market, low freight rates, and a strong retail market are reasons to cheer for the retail businesses, the producers’ price index (PPI) for freight trucking continues to remain well above pre-pandemic levels.

With freight prices not expected to fall further, Muenster contended that a bulk of this increase is tied to the high labor costs. “The cost of equipment isn’t increasing as it did during the pandemic, freight rates are down, capacity is easy to come by, but labor continues to drive price pressure across the industry.”

The Week in Snippets

US truckload carriers are grappling with a continued slump in demand, leading to reduced rates and revenues, with major players like Landstar and Covenant Logistics experiencing significant drops in revenue year over year. Despite the optimism earlier in 2023, high inventory levels and flattening spot rates paint a bleak outlook. However, some industry leaders, like Knight-Swift's CEO Dave Jackson, anticipate a potential uptick in demand by the year-end holiday season.

Amazon's drone delivery initiative, Prime Air, has faced a major setback with the departure of two key executives, Jim Mullin and Robert Dreer. This comes amidst already existing challenges for the program, including regulatory restrictions and operational hurdles, which have considerably delayed its rollout since Jeff Bezos's 2013 predictions. Additionally, a recent major layoff by CEO Andy Jassy further impacted Prime Air's development and objectives.

Due to drought-induced water conservation measures, the Panama Canal is facing significant congestion, with a current wait time of around 21 days and 154 vessels queued. As the U.S. represents 73% of the canal's traffic, these delays could heavily impact trade, especially since the booking slots for large Panamax vessels have been notably reduced. The disruption poses substantial risks to global supply chains and U.S. trade activities.

Hapag-Lloyd reported a 77% decrease in Q2 net profit to $1.1 billion, attributing the decline to weaker demand and unsustainable freight rates. CEO Rolf Habben Jansen mentioned that returning to pre-pandemic freight rates would mean operating at a loss due to increased operating costs on certain routes. Despite these challenges, the company, which recently acquired Chilean firm SAAM Ports & Logistics, is looking to further expand its terminal business.

Quotable

“SoCal is the canary in the coal mine for the U.S. industrial market to some extent.”

- Mark Russo, head of industrial research at real-estate services firm Savills, commenting on the cooling warehousing market in Southern California over the first half of ‘23.

Like what you read? Do consider subscribing! Have something you’d like me to cover? Reach out at vishnu@storskip.com